Democratizing the World of Venture Capital

Jonathan Medved

Founder and CEO, OurCrowd

Since its inception in 2013, OurCrowd has been committed to democratize access to venture capital while maintaining best venture practices for a new class of investors.

The opportunity and time for OurCrowd’s innovations are driven by a number of factors. These include consistent high returns in the asset class, which nevertheless have benefitted only a small subset of investors; increasing difficulty in accessing the best deals, as top deals stay private longer and then IPO at extraordinary valuations. On top of the above, all but the most sophisticated investors have not been granted standard economic preferences, which are critical to offset risk and preserve upside.

Opportunity and Differentiation

Compared to other seemingly similar “crowdfunding” platforms, the OurCrowd platform is distinguished in a number of ways. Testimony to its vision and success in education, it currently has 40,000 accredited investors from over 180 countries who access highly curated individual venture deals and venture capital fund. The emphasis is on investing relatively large amounts from aggregated individuals and institutions via an LP/ GP structure. Median check size is $3.5M per portfolio deal, with many companies raising amounts beyond $10M.

If growth opportunities have shifted — not all the way, but to a substantial extent — into private markets and ordinary investors don’t have access to them, that’s not good... It’s hard to give individuals access to private markets. Can we have a fund structure to ensure that ordinary investors are getting the same deal?

Jay Clayton Chairman US Securities and Exchange Commission September 19, 2019

OurCrowd has already invested in over 200 portfolio companies and 19 funds, and has had 36 portfolio exits to date, including leading companies such as Beyond Meat (BYND), JUMP Bikes (sold to Uber), Wave (sold to H&R Block), and Argus (sold to Continental).

OurCrowd often leads its deals; invests alongside leading venture funds; gets Board seat representation in a majority of its deals; purchases preferred stock; and receives anti-dilution protection, pre-emptive rights and liquidation preferences – just like traditional venture investors.

The model has proven successful thus far. OurCrowd has been recognized by Pitchbook since 2014 as the most active venture investor in the highly competitive Israeli venture market, achieving this status only one year after its launch.

OurCrowd – and the idea behind it – might have reached the market at the right time.

Democratizing Access to Venture Investing – and Offsetting Risk

Venture capital as an asset class has performed well for its investors over the decades, in fact generally outperforming all other asset classes. And yet, it has been the most esoteric, most inaccessible asset class even for many large institutional investors. The number of institutions that have significant commitments to venture is actually rather limited; accredited and ordinary investors can only dream. Yet, particularly as fast-growing companies stay private longer and seem to take forever to go public, it is clear that the need to open up access to this closed club of venture investing is becoming imperative. The question is how to execute on this “democratization” in a way that will both benefit the venture ecosystem and the companies it serves, as well as provide compelling returns and protections for a broad range of new investors.

Jay Clayton’s galvanizing call to democratize access to venture is understandable given the history. As the table below shows, the 25-year IRR for Venture top- quartile performance averages 31%, far exceeding Private Equity’s 13%.

Comparative Returns by Asset Class

| Asset | 5-Year | 10-Year | 15-Year | 20-Year | 25-Year |

|---|---|---|---|---|---|

| Venture Capital | 13% | 13% | 11% | 21% | 31% |

| Private Equity | 12% | 14% | 13% | 12% | 13% |

| Real Estate | 11% | 8% | 7% | 7% | 8% |

| Large-cap Equity | 10% | 13% | 8% | 7% | 10% |

| Bonds | 3% | 3% | 4% | 5% | 5% |

- Venture capital (VC) involves investment in start-ups, often with new business models and products, which have potential for significant growth

- Average returns (IRR) for venture capital have historically exceeded those for other asset classes

Source: Pitchbook. Notes: 1. Cambridge Associates Global Venture Capital, Global Private Equity, and Global Real Estate Benchmarks Return Report. Private equity asset class excludes venture capital, 5-,10-, 15-, 20-, and 25-year returns representative of average pooled IRR for vintages dating back from 2014. Top quartile returns for all asset classes shown. Large-cap equity proxy is Lipper aggregated US large- cap equity fund performance. High yield bond proxy is Lipper aggregated high yield bond fund performance. Aggregate core bond proxy is Lipper aggregated core bond fund performance. Returns as of Dec. 31, 2015. Sample size for each asset listed is as follows: venture capital: 91–440; private equity: 174–630; real estate; 71–207; large-cap equity; 62–674; high yield bonds: 30–421; and aggregate core bond: 22–385.

Increased commitments to venture capital

and the formation of mega funds – like the $100B Softbank Vision Fund – have

driven dramatic growth in venture capital investments globally

JUMP Bikes – aquired by Uber in April 2018

Yale University Endowment, a leading institutional investor led by the legendary David Swensen, over the years has “captured great value from the illiquidity premium of alternative assets” and made outsize commitments to Venture Capital as part of a fundamental core of its asset-allocation strategy. In fact, Yale has announced that it is upping its commitment to Venture Capital to a whopping 21.5% as target for 2020.

Yale’s endowment allocation to venture capital continues to grow

| 2018 Actual | 2020 Target | |

|---|---|---|

| Absolute return | 26.1% | 23.0% |

| Venture capital | 19.0% | 21.5% |

| Leveraged buyouts (Incl. PE) | 14.1% | 16.5% |

| Foreign equity | 15.3% | 13.8% |

| Real estate | 10.3% | 10.0% |

| Bonds and cash | 10.3% | 7.0% |

| Natural resources | 7.0% | 5.5% |

| Domestic equity | 3.5% | 2.8% |

| Total | 100% | 100% |

Yale’s Endowment Allocation, considered one of the premier endowment models, continues to maintain a well-diversified, equity-oriented portfolio with

a growing share allocated to Venture Capital.

Surpassed $30B mark as of June 30th 2019

These increased commitments to Venture Capital and the formation of mega funds – like the $100B Softbank Vision Fund – have driven dramatic growth in Venture Capital investments globally, rising from $175B in 2017 to over $255B in 2018. In Israel, one of the world’s Venture Capital hotbeds, the growth rate in venture investments has been even more impressive, rising from $2.4B in 2013 to $6.4B in 2018, with more than $8B projected to be invested in 2019.

This funding bonanza has led companies to stay private longer and put off their eventual public offerings until they have long crossed over into “Unicorn” status (start-ups with a valuation of at least $1B). This extended Unicorn runway reduces the eventual returns offered to investors who buy the IPOs when they ultimately go public.

Given the influx of capital into private companies, companies are now delaying their IPO until much later in their lifecycle – significantly limiting returns once they are public.

Source: OurCrowd, as at June 13, 2019

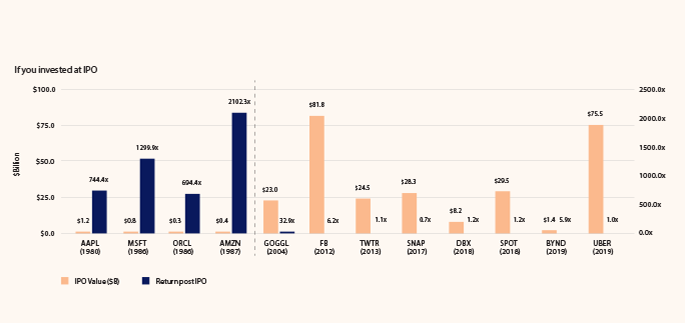

As an example, the number of Unicorns significantly increased in just 14 months, from 279 in February 2018 to 452 in May 2019, and had a combined valuation of $1.6T. This was demonstrated in a striking manner by renowned venture investor Mark Andreesen when he compared the returns offered to public investors in the “good old days” when they invested in the IPOs of Microsoft, Apple, Amazon, and Oracle vs. today when IPOs such as Uber already had an $82B offering value (since down over 30%) and investors refuse to support the prices of over-inflated IPOS, famously tanking the planned public debut of WeWork at $47B. Frustrated investors, both individual and institutional, are asking why they were not able to invest together with the lucky few in Uber’s $1.3M angel funding round.

Net net, the problem is that unless one is lucky and well connected enough to be “invited” to join such a round, getting into quality Venture Capital deals and funds is very difficult. As an individual, participation in angel funding is totally dependent on who one knows, and is very localized. If you live in Silicon Valley and are a VC or senior member of a Google or Facebook team, you may get shown angel deals. But if you are a wealthy dentist in Peoria, Illinois, your chances are pretty much non- existent. Even the wealthiest individuals or family offices who are willing to pay the usual minimum $5M LP entry ticket and get into quality Venture funds have a very tough time getting allocation. The waiting list to invest in Benchmark, First Round Capital and others is akin to an infinite loop.

Institutions also have to build teams of investors to hunt these funds and fight for allocation often only to settle for a $5M–10M LP piece in an untested fund, which needs to be multiplied by 20 other different fund commitments in order to invest a $100M–$200M amount representing only 1%–2% of a $10B corpus. The need to rinse and repeat this allocation hunt every three- four years according to each fund’s launch and funding schedule proves daunting to all but the most committed asset allocators, thus leaving many wannabe institutional venture investors left out in the cold.

Increasing the Investment Public’s Access to Venture Capital

There have been a number of initiatives launched over the past several years to address this limited access to venture capital. AngelList is a popular site that allows individual accredited angel investors to join with other angels in syndicates formed to back deals listed online. AngelList splits a carried interest (typically 20%) with the lead angel (syndicate leader) and, generally, no ongoing management fees are charged. While some of the angels and their deals are of good quality, there is no overall supervision or curation of deals, and the quality of some listed deals is often spotty. Moreover, the angels are not necessarily taking board seats, nor always buying preferred stock, nor focused on providing added value to the company, or even allowing for follow-on investment opportunities.

Several sites that were promulgated in response to the JOBS Act of 2012 (Regulation Crowdfunding sites, or Reg CF, according to the SEC regulations), allow for even non- accredited investors to join in online venture deals. However, the amount of capital that Reg CF sites can invest is limited to $1M per company and the sponsors of the sites make their money as a kind of junior broker dealer, being paid by the companies a percentage of capital raised. Stock is directly owned by the individual investor so, potentially, hundreds of investors are added to a company’s cap table.

Even the wealthiest individuals or family offices... have a very tough time getting an allocation. The waiting list to invest in Benchmark, First Round Capital and others is akin to an infinite loop

Crowdfunding Platforms

| Platform | Curation | Stock type | Board seats | Follow on | Fees |

|---|---|---|---|---|---|

AngelList | By Angel | Generally common | Generally not | Generally not | 20% carried interest |

Regulation Crowdfunding | Little or none | Common | None since regulations prohibit | None | Slotting/broker fees from companies |

OurCrowd | Standard Venture Diligence | Preferred | In majority of cases where available | In most cases | 2% management, 20% carry |

The stock purchased is generally common shares, without anti-dilution or pre-emptive rights, no platform supervision, no board seat, nor follow-on investments. These Reg CF investors are the first investors to be hurt if there is a “down round” (financing at a lower valuation) and the first to be left out if there is an “up round” (financing at a higher valuation).

Given that companies must pay the Reg CF to be listed and upon success, and that sponsors do not invest their own capital in the portfolio companies, the companies selected are subject to a negative selection bias, with Reg CF generally choosing companies that can’t raise money from recognized Venture Capital investors. Clearly, an alternative for individual investors, which rewards rather than penalizes their participation, is necessary. OurCrowd seeks to provide such an alternative. (See table opposite)

OurCrowd’s financial model employs the standard 2/20 Venture manager profit share (2% management, 20% carried interest), thus aligning interests between investors and the platform. However, minimum investment sizes are modest: $10,000 for individual companies and $50,000 for venture funds. Aggregated LP checks for funds already exceed on average $10M per fund.

OurCrowd and Funded Companies: Challenges and Further Opportunities

OurCrowd deviates from regular venture practice in several key areas. First, the companies must help with the fundraising by appearing at face-to-face investor events and roadshows, online webinars and participation in personal calls and meetings with significant investors, family offices and institutions. This creates a linkage between the companies and the LPs that is different in kind and intensity from the traditional Company-VC- LP relationship. This differentiated approach becomes a force multiplier factor for portfolio companies because the global investor network can be leveraged to provide strategic introductions, hiring, local distribution and joint ventures, and assistance with follow-on funding. The OurCrowd global network is engaged in real partnership with the companies and thus, paradoxically, OurCrowd is perceived by many of its portfolio CEOs as the company’s most active venture investor.

One of the key challenges faced by platforms that raise funds for individual venture deals the way OurCrowd does, is the general inability to give a firm and hard commitment on the amount of capital to be invested in the company. This, of course, is subject to the success of the funding effort and campaign. However, given overall performance and transparency in the process, this obstacle has been largely overcome (though not yet completely). OurCrowd is hard at work on several new methods to bridge these gaps.

One positive surprise with the OurCrowd funding approach has been the general success of providing follow-on funding to those companies making steady progress, and even in some cases where down rounds occur and trouble needs to be worked out. While this was not at all assured in early plans and discussions, it turns out that in many cases OurCrowd has built its position in subsequent investment rounds, growing from an initial investment of only $1M–$2M in some cases to over $10M as a result of participation in several follow-on rounds. Moreover, since investments are not limited to a single, hard limited fund with issues of reserves and fund lifetime, the potential for follow-on is actually quite significant, especially if the global LP network is engaged with the company.

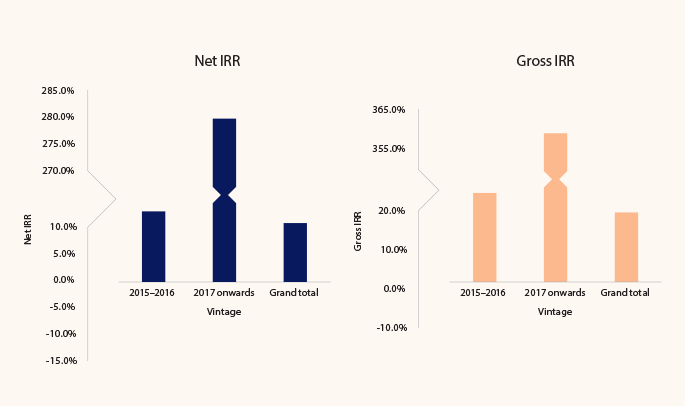

OurCrowd’s Returns based on 51 concluded investments (i.e.: Exits & Write-offs) – IRR

Returns have been calculated internally by OurCrowd, based on IPO prices as at 6.30.19, and have not been independently audited.

OurCrowd is also different in its approach to Corporate Venture partners that are registered on the platform in order to engage with portfolio companies; perform Proof-of- Concept testing (POCs); and even contract for paid scouting and other innovation services, including Corporate VC as a service. Over 1,000 multinationals are registered on the platform, thus providing additional value to the portfolio companies and funds.

OurCrowd is both a direct investor in companies and in funds and, therefore, also has a different scale than most Venture organizations. These funds are either built by teams hired by OurCrowd, or as theme- or strategy-driven portfolios selected from among its direct investments, or as partnerships built with other venture funds that allow OurCrowd to invest as an LP in their funds. Leading funds such as USVP, Maniv, Proof, OXX, and others have received significant LP funding from OurCrowd. The ability to choose from a menu of leading Venture Capital funds, which at any given time includes five or more that are currently funding, is a unique offering to both individual and institutional investors who are writing checks and making commitments ranging from $50,000 to many millions of dollars. The fact that there is no “fund of funds overage” (a standard additional 1% management fee and 10% carried interest fees tacked onto the 2/20 model in most fund of funds) is unique and allows OurCrowd investors to build their own diversified venture fund portfolios.

| Year | Met IRR | Gross IRR |

|---|---|---|

| Vintage 2015-2016 | 12.9% | 22.2% |

| Vintage 2017-2018 | 282.8% | 355.2% |

| Grand total | 32.6% | 42.5% |

Looking into a More Democratized Future

The key factor that will ultimately make or break democratization of Venture Capital is performance. Can the new platforms bringing new investors to the asset class deliver the results needed to justify the inherent risk and illiquidity of venture investments? While it is still early and much work and analysis need to be done, OurCrowd’s initial results are promising.

Overall performance in certain key performance criteria such as DPI (distributions as a function of paid-in capital) are already exceeding top-quartile benchmarks from Cambridge Associates. For the sake of analysis, we looked at all investments in company SPVs in aggregate as three- year funds (2013 and 2016 funds) and both exceed the DPI measurement needed to enter the coveted top-quartile cohort.

Moreover, performance is improving over time as the model continues to prove it can deliver for companies and investors. Earlier company cohorts in the 2013/2014 time frame were not the best performers, but the quality of deal flow has improved markedly as value is added consistently to the portfolio and performance is delivered for investors. Analysis of the performance of “completed investments,” including all exits and write-offs, shows dramatic improvements since inception.

OurCrowd has launched a fund called OC 50, which is a kind of Venture Index fund consisting of a portfolio of 50 different companies. For each $50,000 fund increment, an equal amount of $1,000 per company was invested in a multi-vector diversification strategy. The 2017 vintage portfolio was invested across sectors, stages (from early to late), and geographies. The performance to date has been striking with five exits (two from Israel, two from the U.S., and one from Canada) and top performance across several key metrics.

This kind of performance is bringing attention from institutions that now wish to broadly distribute these products to their clients who otherwise have no access to the Venture Capital asset class. On Oct 16, 2019, Stifel, a leading U.S. diversified financial group that is the 7th largest U.S. broker dealer and has the country’s largest equity research platform, announced a strategic deal with OurCrowd.

The OurCrowd Global Investor Summit 2019

The deal includes an investment in OurCrowd and a decision to distribute OurCrowd products to its over 1 million clients through the firm’s 2,200 financial advisors. This is the first time a major U.S. financial institution has announced an intent to broadly distribute Venture Capital products and will have major ramifications on both OurCrowd’s business and reach, as well as the broader financial markets.

It seems that the democratization of access to Venture Capital is already taking shape. Let us hope that these are the first of many moves that will allow broader and successful access to Venture Capital among both institutions and the individual investor. The advantages to these investors, as well as to the companies they invest in, will be a game changer.

Looking forward, I think you’re going to see a whole bunch of initiatives to bring more and more people into the asset class.

About the Author

Jonathan Medved is a serial entrepreneur, one of Israel’s leading high tech venture capitalists, and was named one of the world’s “50 most influential Jews” by Jerusalem Post.

Medved is the founder and CEO of OurCrowd. He was the co-founder and former CEO of Vringo; the founder and general partner of Israel Seed Partners; a founder and executive VP of marketing and sales at MERET Optical Communications, Inc.; executive VP of marketing and sales at Accent Software.

Medved has served on the Boards of Ma’aleh Film School, Michael Levin Lone Soldier Center, Artists and Musicians for Israel, Bnai David Eli, and served on the Board of Governors of the Jewish Agency and the Jerusalem College of Technology.

Medved is a frequent guest and commentator on television and was featured in several documentary movies. His writing has appeared in the Wall Street Journal, USA Today, The Jerusalem Post, and Townhall.com.